Maxed Out Nation

The Fed's Rate Cuts Make No Sense If the Economy Is as Strong as They Say

Lately, I've been focused on writing about all things gold, and I haven't had the chance to properly dive into something I've been itching to address since last week: the Federal Reserve's pivot.

As you probably know, after pretending to fight their self-inflicted inflation mess for over a year, the Fed finally threw in the towel. And they didn’t just dip their toes in; they went straight for a 0.5% rate cut.

Now, if you’re like most people, you probably didn’t expect the Fed to kick off its easing cycle with such a significant cut.

Honestly, it makes no sense for the Fed to cut rates so aggressively if everything is hunky-dory. Though they’re certainly keeping up appearances.

Here’s what Federal Reserve Chair J. Powell said during his press conference following the Federal Open Market Committee (FOMC) meeting when asked about his direct message to the American public:

The U.S. economy is in a good place, and our decision today is designed to keep it there. More specifically, the economy's growing at a solid pace, inflation is coming down closer to our 2% objective over time, and the labor market is still in solid shape. So our intention is really to maintain the strength that we currently see in the U.S. economy, and we'll do that by returning rates from their high level…to a more normal level over time.

Hmm… So, no victory over inflation, and yet the Fed has pivoted—even though the “economy is strong”—and in such a big way, no less. Make it make sense. I mean, wasn’t the Fed supposed to keep rates high until they hit their (arbitrary) 2% inflation target?

I guess that’s optional now.

This alone suggests that the FOMC's decision to go for a jumbo rate cut doesn’t really align with Powell’s claims about the robustness of our economy.

My guess - which I suspect will be validated sooner rather than later - is that the Fed knows something's seriously off in our economy, and they're rushing to patch things up before it gets worse.

And the evidence of these problems is hiding in plain sight.

Drowning in Debt

One of the biggest signs that our economy is a lot weaker than Chairman Powell would like us to think is debt.

I’m not talking about government debt, which is a whole other can of worms I've opened up in these pages many times before, but consumer debt.

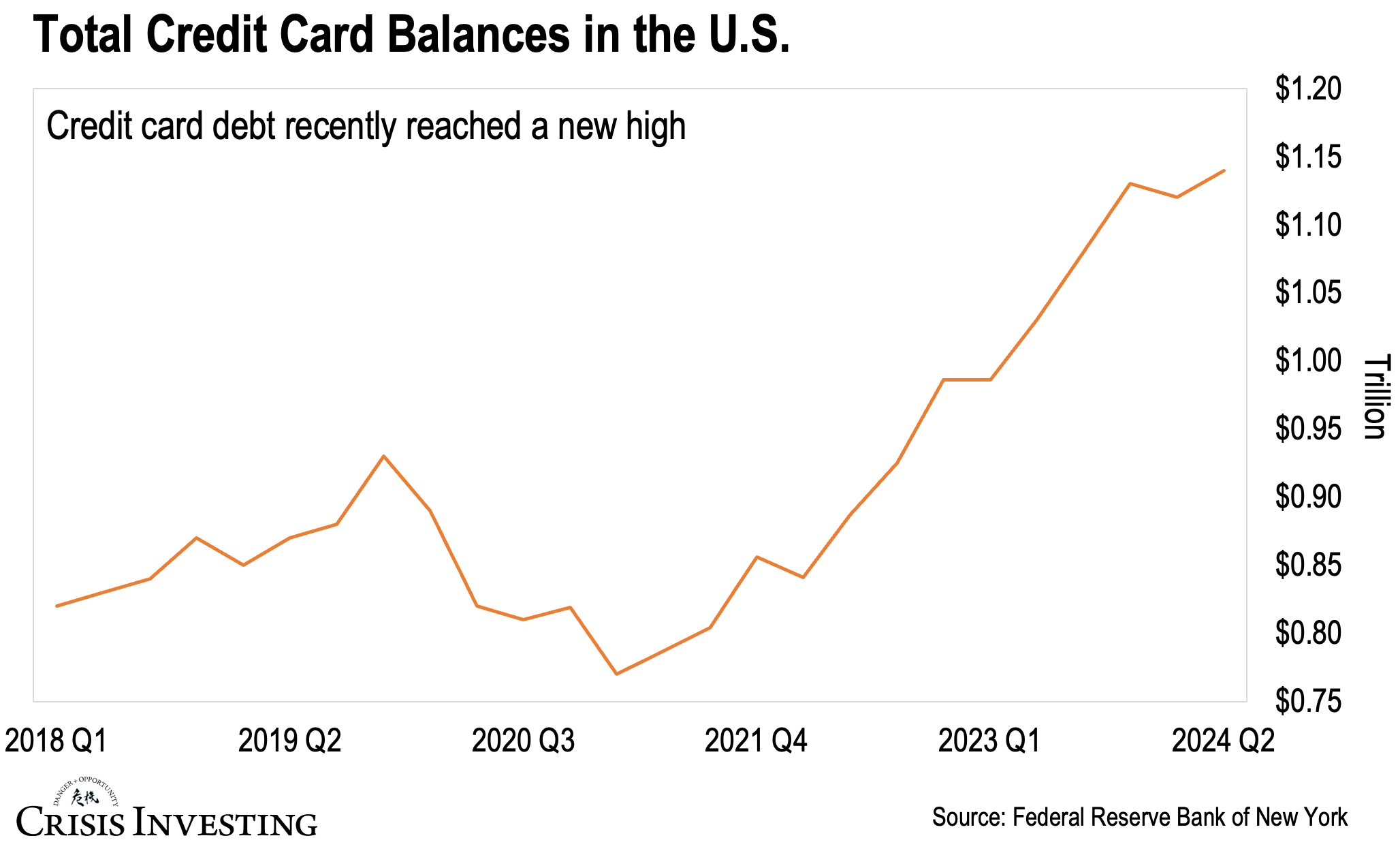

The truth is that American consumers are drowning in a sea of debt, with total credit card balances hitting $1.14 trillion in the second quarter of 2024. That’s according to the latest consumer debt data from the Federal Reserve Bank of New York.

This is the highest balance on record since 1947, having surged during the pandemic and continued climbing ever since. Take a look at this insane spike in the visual below!

Now, this isn't a sign of confidence in the “strong economy”—far from it. It’s a desperate attempt by consumers to keep their heads above water in an economy where wages haven’t kept up with the cost of living.

This situation alone leads me to outright reject the Fed’s claim that all is well.

Savings Crisis

Now, keep in mind, the American consumer debt bubble extends beyond just credit cards. Student loan debt is sitting at around $1.6 trillion, auto loan debt is about the same at $1.62 trillion, and mortgage debt is closing in on $13 trillion. All three are at or near historical highs.

But won’t the Fed's rate cut provide some relief to these overburdened borrowers?

Yes, but the reality is we’re sitting on a powder keg of debt, and the Fed's response is to make borrowing even easier. It’s like treating alcoholism with happy hour specials. This is why any relief that results from this will only be short-lived for most people.

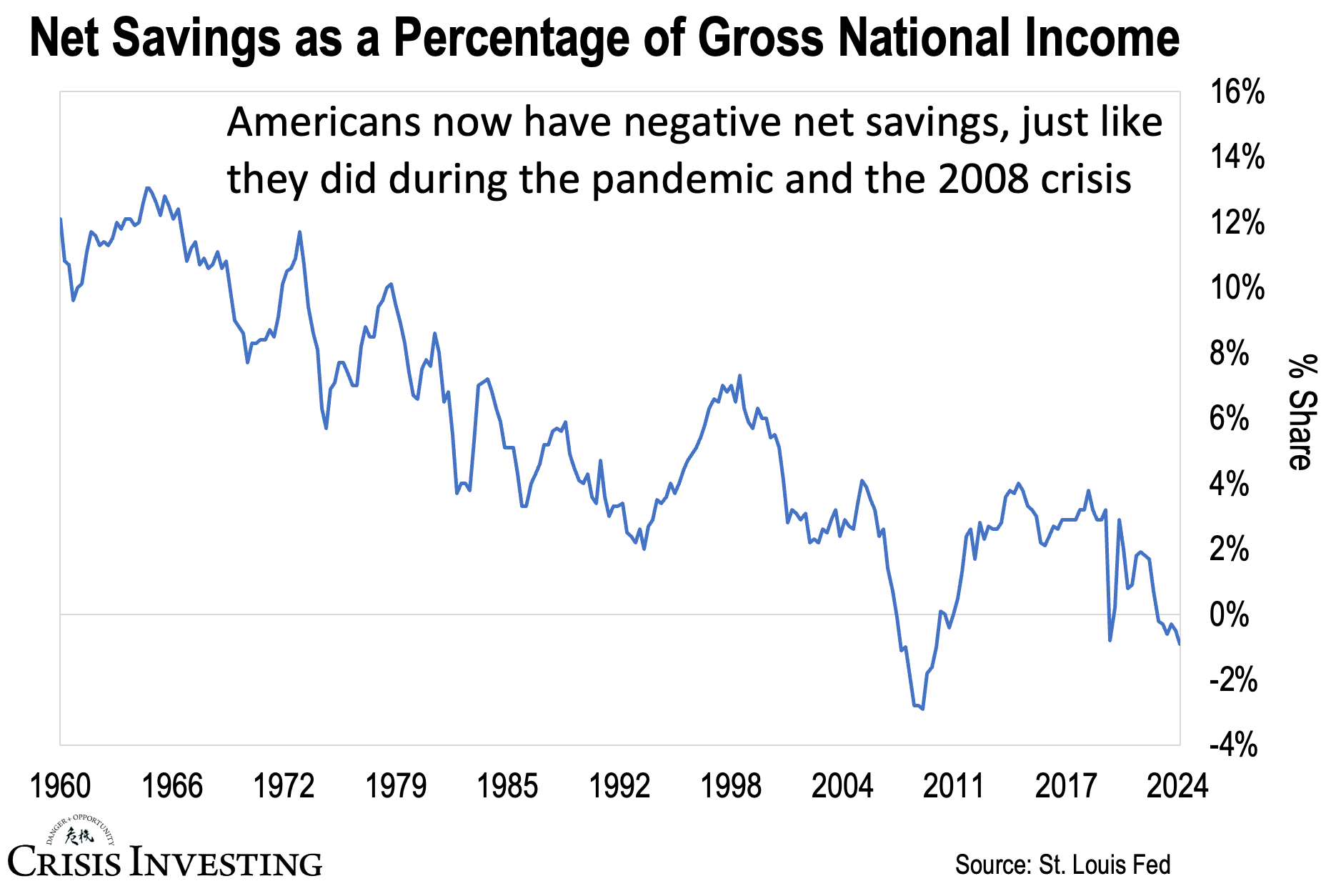

But here’s something that makes me think the Fed might be rushing in with a life raft a bit too late. Take a look at the chart below. It shows U.S. national savings as a percentage of gross national income since the ‘60s. If you look closely, you’ll see that our savings have recently turned negative.

Note: When net savings turn negative, we start spending more than we earn. This overspending happens as individuals, businesses, and the government drain their savings or rack up debt to consume beyond their means. It’s a warning sign that a nation is living large on borrowed time.

Here’s why this matters: in all these decades, there have only been two times this has happened—the Global Financial Crisis of 2008 and the COVID-19 lockdowns in 2020.

So what does it say that the only other times this has occurred were during major disasters?

Well, it means we might be pretty close to one right now. A situation that's very different from the picture the Fed's talking heads are trying to paint right now.

I’ll leave you with some words of wisdom from Doug Casey.

Saving means taking the excess of what you produce over what you consume and setting it aside. It’s basic and essential, because it creates capital. It is capital, in turn, that allows you to advance to the next level. An individual or a society that doesn’t save will soon find itself in trouble.

Regards,

Lau Vegys

P.S. Doug Casey believes that the Fed's decision to cut rates and increase the money supply will create a bubble in commodities, particularly in monetary metals like gold and silver. That's why a significant portion of our Crisis Investing portfolio focuses on these stocks, which Doug himself owns.

Another good read. It also explains why I can’t seem to put any money into savings, other than my 15% to my 401k, even though I’m making more money than I ever have previously. Let’s face it, our grocery bills are literally 3 times what they were in 2020, the electric bill is up at least 30% and fuel for the car is up at least 50%. Oh, and insurance is up about 20% as well. A lousy half point cut from the Fed will not stimulate much of anything, other than another increase in these prices. Allowing a super-size, corrupt banking cartel to set interest rates while at the same time selectively deciding what items are allowed into inflation calculations is problematic. I think Alex Jones is right, the Globalists are getting more desperate as their system is heading for disaster.

<<It’s like treating alcoholism with happy hour specials>>

I chuckled at this. Spot on!