Never Mind that Mountain (of the Fed’s Cash)

Chart of the Week #33

The Federal Reserve has already cut rates twice this year. And by all indications, another cut is right around the corner—markets are pricing in a 97% probability of another 0.25% rate cut next week.

That's quite a swift turnaround... especially considering that the Fed's attempts at tightening have hardly been a success.

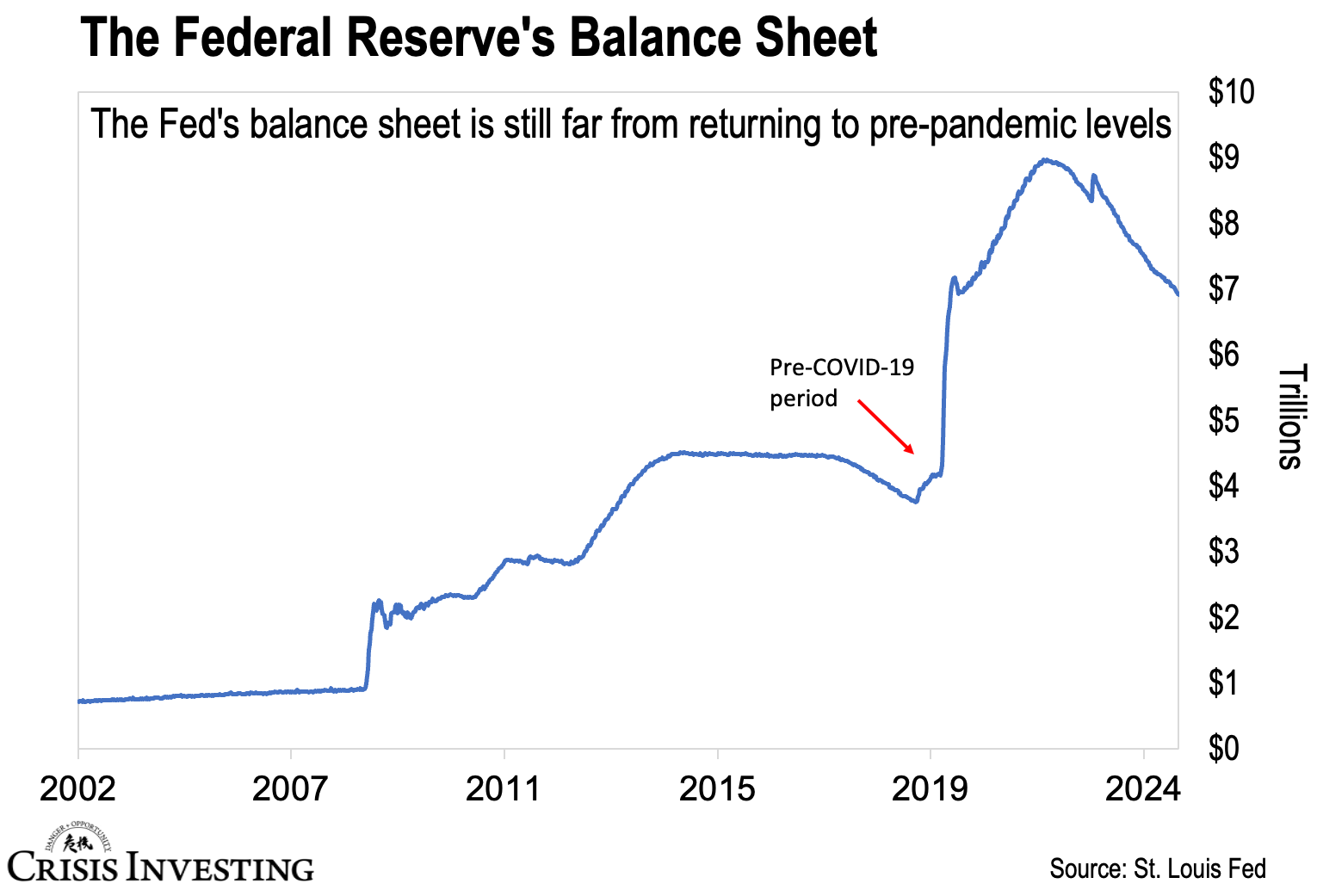

Keep in mind, the Fed is still sitting on nearly $7 trillion worth of assets – the result of its aggressive quantitative easing (QE) program, where it essentially created money out of thin air to buy bonds from banks.

If you remember, the Fed went absolutely berserk with this during the pandemic—flooding banks with cash like there was no tomorrow. By the time it was all over, the balance sheet had blown up to a record $9 trillion.

Since mid-2022, the Fed’s been trying to tighten things up and shrink that massive balance sheet. But after more than two years of QT, they’ve only managed to cut it by about 22%. This week’s chart tells the story.

To say that it's unimpressive would be a gross understatement. But it’s by design.

The simplest way to reverse QE would have been for banks to return the money to the Fed in exchange for their bonds. But that was never going to happen. The Fed and the big banks seem quite content letting all that cash slosh around Wall Street (pushing the market to over 50 all-time highs this year).

Another option would have been for the Fed to sell bonds directly into the market. But they know that dumping a significant portion of their $7 trillion bond portfolio could crash the bond market.

So instead, the Fed chose the gentlest possible approach: letting bonds “roll off”—which simply means not reinvesting the proceeds when bonds mature. It's like trying to drain a swimming pool by waiting for the water to evaporate.

In other words, this whole tightening campaign has largely been theater.

And now, remarkably, with its pivot back to rate cuts, the Fed seems to be saying, "Forget about that mountain of cash still sloshing around in the economy—let’s get ready to fire up the money printer again."

This is a ticking time bomb waiting to go off. Here’s why.

As I wrote to you earlier this week, Trump’s presidency is almost guaranteed to fuel inflation. But with so much money still floating around in the system, that risk goes from bad to worse.

Think about it: when rates drop, all that idle cash doesn’t just sit still—it starts moving as businesses and consumers jump back into borrowing and spending. Throw in Trump’s proposed tariffs—like up to 60% on Chinese goods or 100% on foreign vehicles—and you’ve got a recipe for prices to climb across the board.

Enjoy the rest of your Sunday!

Lau Vegys