The Fed Is Preparing to End Money as We Know It

Big Banks, FedNow, and the Road to Fedcoin

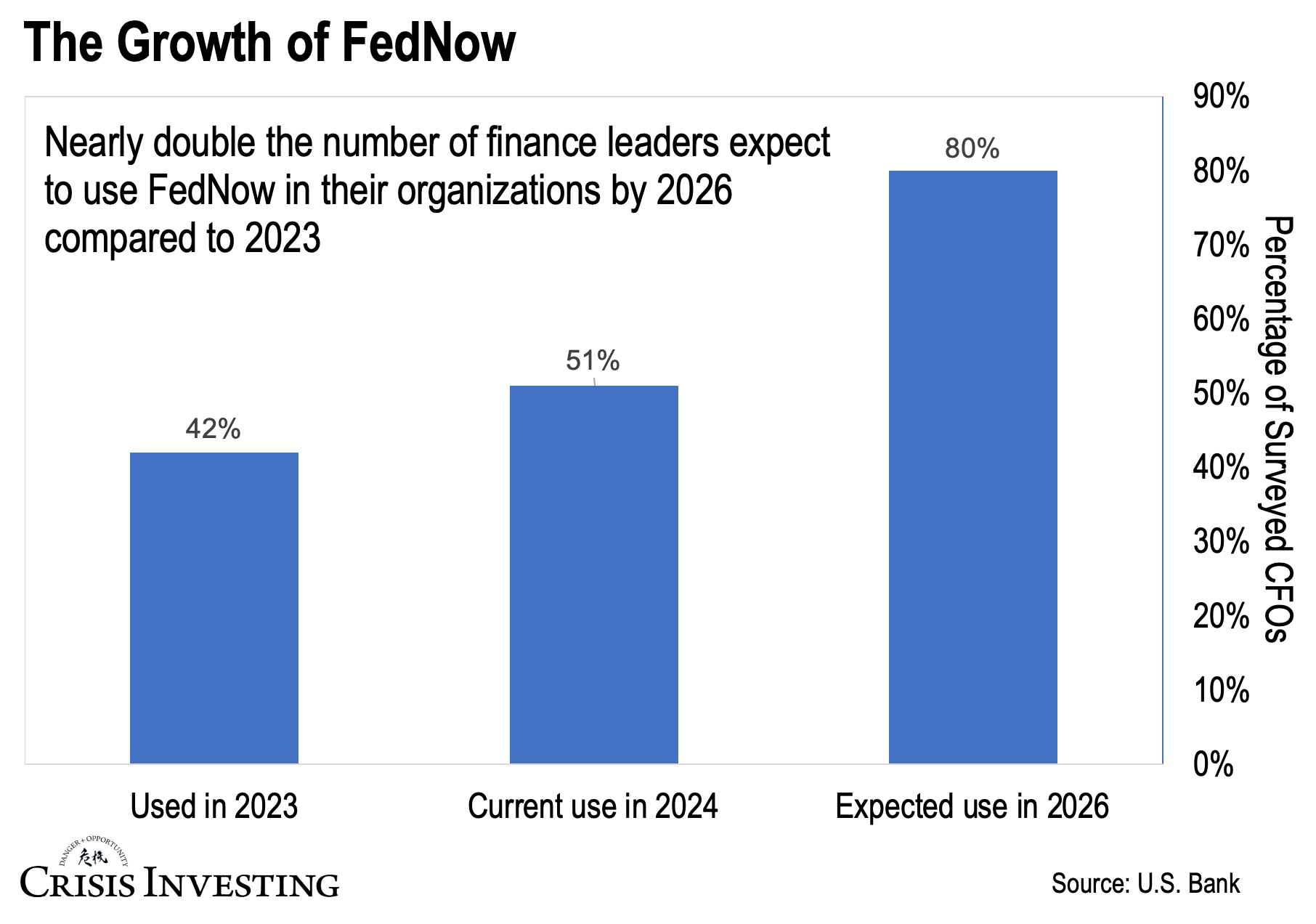

Every quarter, U.S. Bancorp (USB) releases something called U.S. Bank CFO Insights Report. It gathers insights from over 2,000 senior finance officers (CFOs) nationwide. It might not be everyone's go-to read, but it's a good way to stay abreast of what's happening in the banking industry.

Just a few days ago, they dropped the latest issue, and something immediately grabbed my attention — the survey findings on FedNow, the Federal Reserve's new real-time payments service.

The report showed that 42% of surveyed CFOs had tried out FedNow in 2023. Right now, 51% are using it, and notably, a staggering 80% plan to use it by 2026.

In other words, nearly double the number of finance leaders anticipate using FedNow in their organizations by 2026 as they did in 2023.

Clearly, an all-digital dollar is on the horizon, courtesy of the Federal Reserve and big banks.

I'm talking about a currency that wouldn't be printed but would only exist in cyberspace... but one that would also give the Fed and government almost unbreakable financial control over your life.

Now, FedNow isn’t a central bank digital currency (CBDC). But it’s definitely a precursor to one.

Let's backtrack a bit to understand why.

The FedPal

You see, the Fed and big banks have been gearing up for the eventual rollout of a digital dollar for quite some time now.

As far back as 2017, a consortium including finance giants like Citigroup and JPMorgan initiated a real-time payments network operated by The Clearing House, known as the RTP Network.

This network processed a total of 173 million transactions worth about $76 billion during 2022.

The idea behind the RTP Network has always been to lay the technical groundwork and foster a culture of acceptance for a digital currency. The big banks made no secret of it.

But on July 20, 2023, the financial elites, led by the Fed, took it to a whole new level. Industry giants like JPMorgan, Citigroup and Wells Fargo lined up in support behind the project.

Thus, FedNow was born, the Fed’s own real-time payments service.

Officially, FedNow was meant to be like those instant payment apps you use, but for banks. It enables businesses and individuals send and receive instant payments 24/7, 365 days a year. Sort of a FedPal, if you will.

Unofficially, though, FedNow is setting the stage for an all-digital dollar, or, as Doug Casey calls it, Fedcoin.

Doug Casey: The government will undoubtedly come out with Fedcoin – or whatever they’ll call it – its own cryptocurrency. At that point cash will be an anachronism; everything will be done electronically. Every transaction you make will be trackable… to the penny. The government will be capable of blocking your transactions at the push of a button.

Just the Beginning

FedNow is basically a test drive for CBDCs in banks.

That's why the Fed is keen on rolling it out across the financial sector; they've made that much clear. Here are the words of Ken Montgomery, first vice president of the Federal Reserve Bank of Boston and FedNow program executive:

Availability of the service is just the beginning, and growing the network of participating financial institutions will be key to increasing the availability of instant payments for consumers and businesses across the country.

Expanding the Fed’s payments system to include more institutions, and ultimately reaching the public, is also a strategic move to drum up support for an eventual Fedcoin.

And if you take another look at the chart above, it's clear that they are making significant progress in this area.

Consider that, as of today, nearly 800 organizations are already involved. Back in September 2023, that number was “only” 400.

If you open the official FedNow page linked here, you’ll see some big names on that list — like BNY Mellon, Visa, and those I've already mentioned, such as Wells Fargo, JPMorgan, and Citibank.

And there are plenty of reasons for others to follow. Think faster, more efficient fund transfers and improved liquidity management, just to name a few.

If banks see those “reasons” lining up with their business goals, they'll jump on the bandwagon.

Don’t forget, they have been itching for a shot at the payments game, where fintechs like Venmo and Block’s Cash App have held sway. And FedNow could give them a competitive edge.

What This Means for You?

FedNow already gives the Fed the ability to monitor every financial transaction made along with any data associated with that transaction.

That’s a scary proposition. Just think about it…

With this technology, the financial elites have the power, for the first time ever, to track every dollar you spend.

The Fed will deny it. So will the government. They'll talk about checks, balances, and regulation, but that's the reality. And it's getting us closer to the eventual rollout of Fedcoin, which, with FedNow spreading like wildfire, seems all but inevitable at this point.

Regards,

Lau Vegys

P.S. There are things you can do to get ready for Fedcoin's arrival, which will definitely kick the Fed's money printing into a higher gear (never mind other consequences). Consider investing in hard assets like gold and silver. They have proven to be resilient against every kind of crisis imaginable. Doug Casey, too, always recommends holding gold in your long-term investment portfolio. And if you're after some leverage, we have several precious metal stock picks — ones that Doug himself owns — to capitalize on in our Crisis Investing portfolio.

You will like this podcast on the regulation deception. It is up your alley.

https://spotifyanchor-web.app.link/e/8ewVaIBUuJb